DC tax credit local poverty policy case study

In the District of Columbia, tax policy is more than spreadsheets and years-end filings. It sits at the intersection of poverty, service delivery, and political choice—shaping real lives in an expensive city where families juggle housing, childcare, and wages that haven’t kept pace with rising costs. This DC tax credit local poverty policy case study asks: Can targeted city-level credits, funded by prudent reconfiguration of the local tax code, meaningfully reduce child poverty and improve public services, without tipping the broader budget into instability? The answer, so far, is nuanced, data-driven, and tightly linked to the technical and political hurdles that accompany any major tax reform.

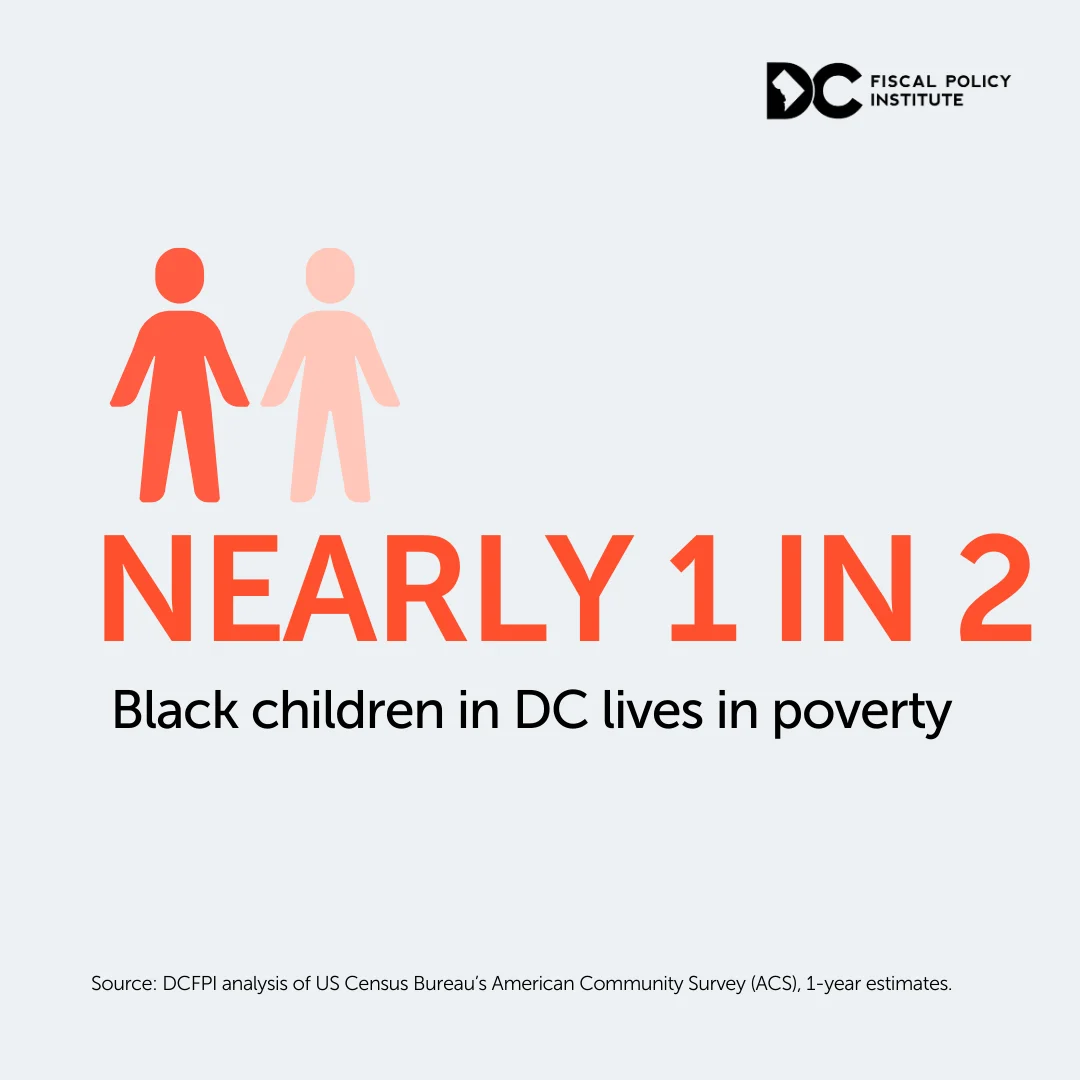

To frame what follows, consider what the city already does and what it planned to do. The District already operates a DC Earned Income Tax Credit that tops out at a substantial share of the federal EITC: for tax year 2024, the DC EITC is 70% of the federal credit, a relatively generous match by national standards. That policy foundation—plus local credits aimed at childcare affordability—formed the backbone of a broader strategy to reduce child poverty and stabilize family finances through tax season. Yet, even with a strong EITC framework, DC’s poverty picture remains stubborn in many communities. In 2024, the official poverty rate in DC stood at roughly 17.3%, with pronounced racial disparities: Black residents faced poverty at about 30.5%, while non-Hispanic White residents remained near the low end of the spectrum at about 4.6%. These numbers, reported by independent policy groups and Census-derived sources, underscore the scale of the challenge and the limits of traditional federal programs in a city with deep structural inequities. (censusreporter.org)

At the same time, city policymakers anticipated a potential strategic lever: a locally funded Child Tax Credit that would supplement the federal credit and reach more families with children, particularly those whose incomes hovered near the eligibility thresholds. By late 2025, the District Council moved to decouple portions of the local tax code from the federal framework, directing revenue toward a local Child Tax Credit of $1,000 per qualifying child and toward an accelerated, full local match for the federal EITC. If fully realized, the plan would push the city toward a more robust anti-poverty toolkit and tighter alignment between public services funding and household resilience. But the plan also faced an aggressive federal counterweight: in February 2026, Congress moved to block the decoupling effort, a decision with potentially substantial revenue and programmatic consequences for the District. The evolving status of this policy decision highlights the central tension of local poverty policy where governance, budgetary autonomy, and federal oversight collide. (dccouncil.gov)

Section 1: The Challenge

The Challenge: Deep-Rooted Poverty in a High-Cost Capital

Poverty in DC is not a simple line on a chart; it is a mosaic of neighborhoods and lived experiences shaped by wage gaps, housing costs, childcare access, and the benefits infrastructure that catches people in and out of poverty during and after tax season. The latest district-focused research shows that, even as the national poverty rate trended downward in 2024, DC’s disparities persisted in stark terms. The official 2024 data show a DC poverty rate around 17.3%, with Black residents experiencing poverty at roughly 30.5% and white residents at about 4.6%—a divergence that maps onto historic segregation and concentrated poverty patterns. These numbers are critical for understanding the potential magnitude of any locally funded anti-poverty policy, because the impact of tax credits is not uniform across districts; it is amplified where job quality, childcare costs, and housing burdens are highest. (censusreporter.org)

The challenge for DC, then, is twofold. First, poverty remains persistent even as overall economic indicators improve. Second, standard federal tax credit programs, while valuable, do not uniformly reach all DC families, especially those with complex income patterns or nontraditional work arrangements. The Local Child Tax Credit concept is designed to fill gaps left by federal programs and to tailor support to the District’s specific demographic and economic profile. In that sense, the DC tax credit local poverty policy case study is less about replacing federal policy than about complementing it with targeted, city-driven resources that can be deployed quickly and measured against local outcomes. This distinction matters because the path from policy design to on-the-ground outcomes requires both robust data systems and political latitude to fund new credits. (dcfpi.org)

The Challenge: Policy Fragmentation and Fiscal Uncertainty

Another central tension is the fault line between local autonomy and federal policy. The District’s plan to decouple elements of its tax code from federal tax changes—the “One Big Beautiful Bill Act” framework—was designed to preserve revenue and repurpose it toward anti-poverty initiatives, including the local Child Tax Credit and an enhanced EITC. In November 2025, the District Council approved measures to decouple and to earmark funds for accelerated EITC matching and for a local $1,000 per-child credit, signaling a bold approach to local poverty policy. The policy also drew strength from a legal framework that allows the local government to implement certain tax changes that do not contravene federal law, a mechanism that the DC Council hoped would deliver faster dollars to families than waiting on slow-state or federal processes. But the plan faced a political counterweight: federal lawmakers and federal oversight bodies signaled opposition to decoupling, arguing that the District should not depart from federal tax rules; when Congress blocked the decoupling, the DC policy’s path to impact became contingent on a legal and political struggle, not just an implementation plan. (dccouncil.gov)

The practical implication for technology and systems is equally urgent. A local CTC program, combined with an accelerated EITC, requires integrated tax processing, clear data flows between city agencies and the IRS, and accessible channels for families to claim credits. The DC EITC remains a critical anchor: for 2024, DC’s EITC is 70% of the federal EITC, a high-match rate that already leaves more money in the pockets of low- to moderate-income workers. The city’s tax authority also notes that the DC EITC refund can be issued in a lump sum or in monthly installments if it exceeds certain thresholds, a feature designed to smooth household cash flow but also to interface with other benefits programs. These design choices, while beneficial to families, add layers of operational complexity that any new local credit must navigate if it hopes to reach all intended beneficiaries. (eitc.dc.gov)

Section 2: The Solution

The Solution: A Local Tax Credit Strategy Grounded in Data

The DC tax credit local poverty policy case study centers on a multi-pronged strategy: (1) formalizing a local Child Tax Credit funded by decoupling the city from selected federal tax rules, (2) accelerating the EITC match to maximize the district’s anti-poverty leverage, and (3) modernizing the tax administration to deliver credits promptly and transparently while maintaining safeguards around benefits eligibility. Taken together, these elements aim to translate policy ambitions into quantifiable outcomes for DC families, especially children, in a city where the cost of living remains among the highest in the country. The centerpiece of the solution is a local Child Tax Credit of $1,000 per qualifying child (under age 18) beginning with tax year 2026, a policy designed to fill gaps left by the federal Child Tax Credit and to focus resources on households earning below defined income thresholds. The legislative and policy language confirms the mechanics: $1,000 per qualifying child, eligibility targeted to lower- and middle-income families, and a plan to scale the credit to up to three qualifying children. The credit is structured to align with the city’s broader anti-poverty objectives and to be funded by the revenue savings realized from decoupling local tax policy from federal rules. (code.dccouncil.gov)

The Local Child Tax Credit: Design, Eligibility, and Targets

The DC Child Tax Credit is designed as a refundable credit, mirroring the principle behind the federal Child Tax Credit but with local tailoring to the District’s income distribution and poverty dynamics. Under the 2026 framework, the credit amount is $1,000 for each qualifying child not yet 18 by December 31, 2025; the structure is designed to be inflation-adjusted in subsequent years. Eligibility hinges on income thresholds to ensure the benefit concentrates on working families and households with modest earnings, with specific limits set for single filers, heads of households, and married filers. The design is intentionally targeted to avoid high-income households that would not need local support, while maximizing reach among families with housing, childcare, and transportation costs that correlate with higher poverty risk. The legal text codifies these aims and sets the stage for an operational rollout. (code.dccouncil.gov)

Acceleration of the Earned Income Tax Credit: A Local Amplifier

In tandem with a local CTC, the plan included accelerating the full local match for the EITC to maximize the anti-poverty impact. DC already matches a substantial share of the federal EITC; the path forward envisioned a more aggressive, timely, and potentially monthly-disbursed EITC stream to households, with a full local match once funding and administration permitted. The city’s EITC framework is critical because it directly affects disposable income for low- and moderate-income workers and thus the demand for local services that buffer poverty. The official DC EITC guidance emphasizes that refunds can be distributed as lump sums or monthly installments if the refund amount is above a threshold, a feature that can help families manage bills more predictably but also requires careful coordination with SNAP and other programs. (eitc.dc.gov)

Administrative Modernization: Data, Access, and Delivery

A core part of the solution involves modernizing how credits are claimed, processed, and monitored. The district’s tax administration network must handle an expanded set of credits, ensure timely refunds, and maintain privacy and security as credits cross agency boundaries. The EITC experience is instructive: the city already uses an electronic tax system, with outreach programs to help residents claim EITC benefits. The modernization effort would extend to the new local CTC, the accelerated EITC, and the associated data-sharing protocols with federal systems for validation and eligibility. The administration’s readiness reflects a broader, nationwide trend toward digital tax administration as a means to increase take-up and reduce errors, but it also raises concerns about privacy, eligibility verification, and potential unintended benefit interactions with other programs. (disb.dc.gov)

Implementation Timeline andFiscal Realities

The timeline for these reforms was ambitious. The DC Council’s November 2025 actions laid out the decoupling plan and the funding path for the local CTC and expanded EITC, aligning with the district’s fiscal projections and revenue estimates. The plan anticipated the first local CTC payments in tax year 2026 (refundable credit, effectively shaping 2027 refunds), with the EITC enhancements following on a parallel track. The timeline is clear, though the political environment shifted rapidly in early 2026. Congress’s February 2026 disapproval of the DC decoupling plan introduced a new layer of uncertainty about revenue streams and program continuity. This changed the practical feasibility of the timeline and required the city to rethink near-term cash-flow scenarios, outreach, and contingency planning for families who rely on these credits. (dccouncil.gov)

The Political and Fiscal Risk Landscape

The policy approach is as much political as it is technical. Supporters argued that decoupling and local credits would deliver direct anti-poverty benefits and strengthen social programs in a city where child poverty remains a pressing issue. Opponents warned of revenue volatility and potential legal challenges tied to federal oversight. The Washington Post coverage, along with the district’s own legislative communications, highlighted the fundamental trade-off: funds redirected to local credits could reduce the city’s vulnerability to federal policy shifts, but a federal disapproval decision could cost hundreds of millions in revenue, destabilizing funding for housing, healthcare, and education programs that families rely on. The evolving status—particularly the federal response in early 2026—emphasizes the risk that policy ambitions outpace the policy environment, a central tension for this DC tax credit local poverty policy case study. (washingtonpost.com)

Section 3: The Results

The Results: Measurable Impacts Where Data Meets Policy

This section assembles the concrete data points available to date, clarifying what is known, what is projected, and what remains uncertain as the policy environment evolves. Because the local Child Tax Credit is new and still subject to federal decisions, much of what follows is a mixture of observed indicators (where available) and credible projections anchored in existing research and policy design.

Metric 1: DC EITC Match Rate and Immediate Cash Flow Effects

- Baseline: The District’s EITC match rate for tax year 2024 stands at 70% of the federal EITC, which translates into a meaningful boost for eligible families relative to federal credits alone. This is one of the strongest district-level EITC matches in the country and serves as the anchor for any local expansion of the credit. (eitc.dc.gov)

- Aftermath and implications: A higher match rate increases the effective refundable credit per household, lifting after-tax incomes and potentially reducing demand for emergency assistance in the short run. The administrative option to issue EITC refunds in monthly installments for refunds over a specified threshold adds predictability to household budgeting but requires tight coordination with benefit programs to avoid unintended eligibility disruptions. This feature is specified in the DC EITC guidance and is part of the operational design that would scale with any local expansion. (eitc.dc.gov)

Metric 2: Local Child Tax Credit Amount and Distribution Plan

- Baseline: No DC-local Child Tax Credit existed in the 2024 tax year. The concept was advanced as part of the decoupling strategy and legislative proposals in 2025. The plan envisions $1,000 per qualifying child (under 18) starting in tax year 2026, with eligibility thresholds designed to target lower- and middle-income households. The law codifies the amount and the age cap, and it anticipates inflation adjustments in future years. (code.dccouncil.gov)

- Target outcomes: The goal is to supplement the federal Child Tax Credit, focusing relief on families with income levels that would otherwise struggle to cover essential costs. The local credit’s $1,000-per-child design is intended to reach a broad base of households with multiple children and to displace a portion of poverty risk at the household level. Policy descriptions emphasize targeting low-to-moderate income groups to maximize poverty-reduction effects while preserving district fiscal stability. The policy’s explicit aim to reach up to three qualifying children further clarifies the distribution scope. (code.dccouncil.gov)

Metric 3: Projected Child Poverty Reduction

- Projections: A credible policy analysis cited by national outlets suggests that the local Child Tax Credit, in combination with enhanced EITC, could reduce child poverty in DC by roughly 25%. These projections are based on Columbia University’s Center on Poverty and Social Policy analysis and have been echoed by national outlets discussing DC’s approach to local child relief. While this remains a projection rather than a measured post-implementation outcome, it provides a useful benchmark for assessing the potential impact of the program. The assertion is widely cited by policymakers and media outlets tracking the DC policy evolution. (axios.com)

- Important caveats: Projections depend on program uptake, outreach effectiveness, and the maintenance of funding streams. The policy’s efficacy will also hinge on its interaction with federal credits and any changes to the broader social safety net. The federal political environment, including potential changes to tax policy or blockages by Congress, could alter the realized impact. The District’s own public statements and legislative language emphasize the need to monitor take-up and adjust outreach accordingly. (axios.com)

Metric 4: Revenue Implications and Fiscal Risk

- Federal pushback and revenue risk: The congressional move to block the DC decoupling plan has clear fiscal consequences for the city. If Congress disapproved the plan, DC could face a revenue shortfall on the order of hundreds of millions of dollars through 2029, which would constrain resources available for housing, healthcare, and education programs. The Washington Post reports indicate the disapproval could cost approximately $600 million through 2029, a number that underscores the scale of the policy’s financial stake and the fragility of relying on federal policy alignment for local anti-poverty programs. (washingtonpost.com)

- Policy counterfactuals: If decoupling is blocked, the District would need to adjust the pace and scale of its local credits, postpone some program expansions, or seek alternative funding channels. This dynamic—policy ambition versus federal oversight—highlights a critical risk that the DC tax credit local poverty policy case study cannot ignore: the success of a local poverty relief strategy may depend as much on federal policy signals as on city budget decisions. (washingtonpost.com)

Metric 5: Reach, Take-Up, and Community Sentiment

- Early indicators of reach: The DC policy area is widely anticipated to reach a broad cohort of families with children, particularly those with lower incomes who historically benefited from the federal EITC and Child Tax Credit expansions during the COVID era. Public statements and coverage suggest the measure’s aim to generate broad take-up and to support families with long-standing poverty risk. The Washington Post coverage of the November 2025 council action and subsequent reporting on the policy’s trajectory provide qualitative indications of community and advocacy interest, as well as political momentum. The reporting also notes that a large share of DC’s children live in households that would benefit from such a policy. (washingtonpost.com)

- Community voices and advocacy: Statements from council members and advocacy groups emphasize the moral and economic logic of a local credit, underscoring the belief that targeted local credits can complement federal policy and boost the District’s anti-poverty toolkit. A representative paraphrase from a public coalition statement underscores the civil society view: “The Child Tax Credit is a powerful anti-poverty instrument,” highlighting the policy’s alignment with broader social and economic goals. While direct quotes from the coalition are widely reported, the central claim remains that the policy’s intent is to reduce child poverty and support families in a city with significant housing and childcare costs. (globenewswire.com)

Section 4: Key Learnings

Key Learnings: What Worked, What Didn’t, and What We’ll Watch

- Policy design matters: The local tax credit concept relies on precise design—credit amounts, income thresholds, and age caps—that determine who benefits and how much. The $1,000-per-child local credit, with eligibility tied to income thresholds and age, reflects a targeted approach designed to reach families with meaningful poverty risk, but it will require ongoing evaluation to confirm whether the design translates into the intended poverty-reduction effects. The relevant legal texts codifying the policy provide the blueprint, but the ultimate test is in the data: take-up rates, changes in poverty indicators, and stability of funding. (code.dccouncil.gov)

- Data systems and delivery channels matter: The policy’s success depends on robust tax administration and data-sharing arrangements that can verify eligibility, prevent fraud, and ensure prompt disbursement. The DC EITC framework demonstrates that the city can administer complex refundable credits and offer flexible refund options, but expanding to a new local CTC adds complexity that will require strong IT governance and customer service capabilities. The existing EITC delivery mechanisms provide a foundation, but scaling them will demand additional investments in digital infrastructure and process oversight. (eitc.dc.gov)

- Fiscal risk demands transparent contingency planning: The federal intervention risk—evident in the congressional move to block decoupling—highlights the volatility of relying on state or city policy to drive anti-poverty outcomes. The cost estimates tied to policy disruption (e.g., a potential $600 million revenue impact through 2029) illustrate why cities pursuing bold local tax reforms must accompany policy design with explicit fiscal risk management strategies and realistic, public-facing communication about timelines and trade-offs. (washingtonpost.com)

- Community impact requires ongoing evaluation: The projected 25% reduction in child poverty is an important signal, but it rests on several assumptions about policy uptake, the interaction of local credits with federal credits, and the stability of funding. Continued evaluation will be essential to validate the projection, quantify the actual effects on families with children, and compare DC’s real-world results with other jurisdictions pursuing similar approaches. The Columbia Center on Poverty and Social Policy analysis, as cited in industry reporting, provides a rigorous baseline for benchmarking future outcomes. (axios.com)

- Political economy shapes scale and timing: The policy’s fate is inseparable from political processes at the federal and local levels. The DC Council’s decisions in 2025 and 2026, coupled with Congress’s intervention, show how quickly policy ambitions can be altered by political currents. The precautionary lesson for other cities is to pursue bold ideas with parallel strategies for funding, governance, and stakeholder engagement to withstand political headwinds. (washingtonpost.com)

Closing

The DC tax credit local poverty policy case study reveals a city attempting to transform its tax code into a straighter line from cash-flow to child welfare. By pairing a local Child Tax Credit with an enhanced Earned Income Tax Credit, the District sought to directly reduce poverty among children while preserving essential public services. The plan’s core logic—targeted relief for those most at risk, funded by revenue saved through decoupling local tax rules from federal changes—reflects a thoughtful, data-informed approach to poverty policy in a high-cost urban context. Yet, the policy’s fate is in flux as the federal policy environment evolves. Reports of Congress’s block on decoupling underscore the fragility of local anti-poverty gains when national policy can shift overnight. As politics and economics continue to intersect in the District, the question remains: will the local tax credits be able to deliver their promised reductions in child poverty, and can the city sustain the investments required to keep those gains durable? The coming years will be a test of policy design, administrative execution, and the endurance of political will. (washingtonpost.com)